Cash Basis Accounting vs. Accrual Accounting

Cash basis accounting and accrual accounting are two different methods used to record and report financial transactions in an organization. Each method has its own approach to recognizing revenue and expenses, and they have implications for how financial statements are prepared and how financial performance is assessed. Let us understand both of these in detail.

Cash Basis Accounting

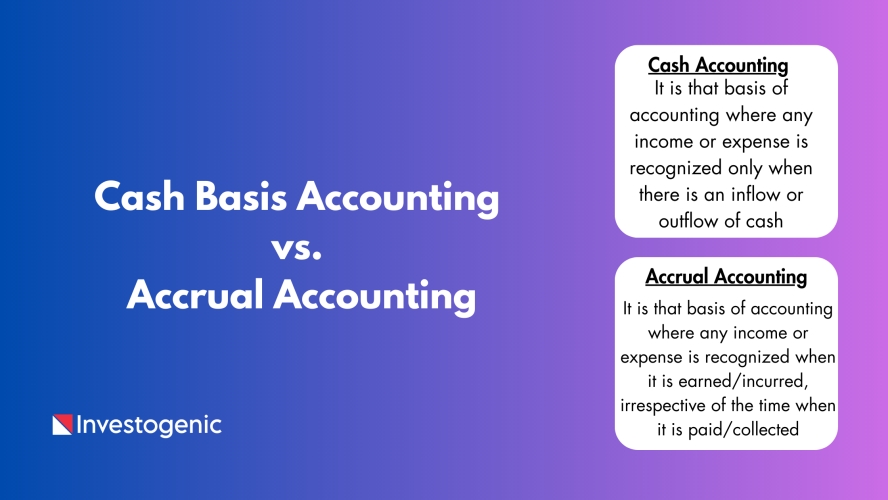

In cash basis accounting, transactions are recorded and recognized when actual cash changes hands. Revenue is recognized when cash is received, and expenses are recognized when cash is paid. This method is relatively straightforward and is commonly used by small businesses and individuals.

Pros:

- Simple and easy to understand.

- Well-suited for businesses with straightforward financial transactions.

Cons:

- May not accurately represent the financial performance or position of a business.

- Does not account for credit transactions or future commitments.

- This can result in timing differences between actual economic activities and their recognition.

- It’s not appropriate for all businesses

Accrual Accounting

In accrual accounting, transactions are recorded and recognized when they occur, regardless of when cash is exchanged. Revenue is recognized when it is earned (goods or services are delivered), and expenses are recognized when they are incurred, even if cash payment has not yet been made. This method provides a more accurate picture of an organization’s financial position and performance.

Pros:

- Reflects the economic reality of transactions, even if cash hasn’t been exchanged yet.

- Provides a more comprehensive view of financial activities.

- Better matches revenue and expenses with the periods in which they are incurred.

Cons

- Can be more complex to implement and understand, especially for non-accountants.

- May require adjustments for items like unearned revenue, prepaid expenses, and accruals.

Example

Let’s say you are a business owner who receives an electric bill of $1,000. Under cash-basis accounting, the amount is not recorded until your business pays the bill. However, under the accrual method, the $1,000 is recorded as an expense on the day the business receives the bill.

The same principle applies to income, such as if a business sold someone $5,000 worth of goods on credit, then in cash-based accounting, the amount is not received until the income or revenue is booked, whereas in accrual-based accounting the $5,000 is recorded as income or revenue on the day the business sells the goods.

Difference between cash basis accounting and accrual basis accounting

The main difference between cash-based accounting and accrual-based accounting lies in the timing of when revenue and expenses are recognized. The cash method provides an immediate recognition of revenue and expenses, while the accrual method focuses on anticipated revenue and expenses. Let’s explore the differences between cash accounting and accrual accounting:

| Differences | Cash Accounting | Accrual Accounting |

|---|---|---|

| Recognization | It is that basis of accounting where any income or expense is recognized only when there is an inflow or outflow of cash | It is that basis of accounting where any income or expense is recognized when it is earned/incurred, irrespective of the time when it is paid/collected |

| Variation in income statement | The income statement will show a relatively lower income | The Income statement will show a higher income |

| Nature | Simple | Complex |

| Accounting system followed | Single entry system | Double entry system |

| Accuracy | Low | High |

| Adopted by | For small businesses | Large corporations and publicly traded companies |

How to Choose Between Cash Accounting and Accrual Accounting

The choice between cash accounting and accrual accounting depends on factors such as the nature of the business, regulatory requirements, and the organization’s size and complexity. It’s important to note that the choice of accounting method can have implications on taxes, financial statements, and business decisions.

- Small Businesses and Individuals: Cash accounting is often favored for small businesses and individuals due to its simplicity and directness. However, as businesses grow or become more complex, they may transition to accrual accounting for a more accurate financial view.

- Medium to Large Businesses: Accrual accounting is generally more appropriate for businesses that have credit transactions, inventory management, and long-term projects. It provides a clearer picture of financial performance, which is important for decision-making and financial reporting.

- Regulatory Requirements: In many cases, regulatory authorities or tax agencies dictate the accounting method that must be used. Some businesses may be required to use accrual accounting, especially if they exceed certain revenue thresholds.

- Financial Reporting: If a business seeks external financing or investment, potential lenders or investors may prefer accrual-based financial statements for a more accurate assessment of the business’s financial health.